|

|

|

Pricing strategies in inelastic energy markets: can we use less if we can’t extract more? |

Alexey Voinov1( ), Tatiana Filatova2 ), Tatiana Filatova2 |

1. International Institute for Geo-Information Science and Earth Observation, University of Twente, Enschede 7522EA, The Netherlands

2. Centre for Studies in Technology and Sustainable Development, University of Twente, Enschede 7522EA, The Netherlands |

|

|

|

|

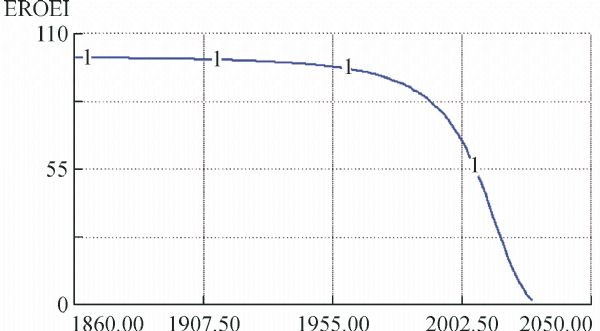

Abstract Limited supply of nonrenewable energy resources under growing energy demand creates a situation when a marginal change in the quantity supplied or demanded causes non-marginal swings in price levels. The situation is worsened by the fact that we are currently running out of cheap energy resources at the global scale while adaptation to climate change requires extra energy costs. It is often argued that technology and alternative energy will be a solution. However, alternative energy infrastructure also requires additional energy investments, which can further increase the gap between energy demand and supply. This paper presents an explorative model that demonstrates that a smooth transition from an oil-based economy to alternative energy sources is possible only if it is started well in advance while fossil resources are still abundant. Later the transition looks much more dramatic and it becomes risky to rely entirely on technological solutions. It becomes increasingly likely that in addition to technological solutions that can increase supply we will need to find ways to decrease demand and consumption. We further argue that market mechanisms can be just as powerful tools to curb demand as they have traditionally been for stimulating consumption. We observe that individuals who consume more energy resources benefit at the expense of those who consume less, effectively imposing price externalities on the latters. We suggest two transparent and flexible methods of pricing that attempt to eliminate price externalities on energy resources. Such pricing schemes stimulate less consumption and can smooth the transition to renewable energy.

|

| Keywords

peak oil

price externality

alternative energy resources

EROEI

|

|

Corresponding Author(s):

Alexey Voinov

|

|

Issue Date: 05 March 2014

|

|

| 1 |

W B Arthur (2006). Out-of-equilibrium economics and agent-based modeling. In: L Tesfatsion, K L Judd eds. Handbook of Computational Economics Volume 2: Agent-Based Computational Economics. Amsterdam: Elsevier B.V., 1551–1564

|

| 2 |

R U Ayres, L W Ayres, B Warr (2003). Exergy, power and work in the US economy, 1900–1998. Energy, 28(3): 219–273

https://doi.org/10.1016/S0360-5442(02)00089-0

|

| 3 |

C Bartusch, F Wallin, M Odlare, I Vassileva, L Wester (2011). Introducing a demand-based electricity distribution tariff in the residential sector: demand response and customer perception. Energy Policy, 39(9): 5008–5025

https://doi.org/10.1016/j.enpol.2011.06.013

|

| 4 |

S C Bhattacharyya (1996). Domestic energy pricing policies in developing countries: why are economic prescriptions shelved? Energy Sources, 18(8): 855–874

https://doi.org/10.1080/00908319608908818

|

| 5 |

W A Brock, A Xepapadeas (2004). Management of interacting species: regulation under nonlinearities and hysteresis. Resour Energy Econ, 26(2): 137–156

https://doi.org/10.1016/j.reseneeco.2003.11.004

|

| 6 |

D S Brookshire, H S Burness, J M Chermak, K Krause (2002). Western urban water demand. Nat Resour J, 2(4): 873–898

|

| 7 |

P Cheshire, S Sheppard (2005). The introduction of price signals into land use planning decision-making: a proposal. Urban Stud, 42(4): 647–663

https://doi.org/10.1080/00420980500060210

|

| 8 |

J Chow, R J Kopp, P R Portney (2003). Energy resources and global development. Science, 302(5650): 1528–1531

https://doi.org/10.1126/science.1091939

pmid: 14645838

|

| 9 |

C J Cleveland, R Costanza, C A S Hall, R Kaufmann (1984). Energy and the U.S. economy: a biophysical perspective. Science, 225(4665): 890–897

https://doi.org/10.1126/science.225.4665.890

pmid: 17779848

|

| 10 |

R Costanza, M Hart, S Posner, J Talberth (2009). Beyond GDP: the need for new measures of progress. The Pardee Papers 4: 46

|

| 11 |

H Daly, J Farley (2004). Ecological Economics. Washington D C: Island Press

|

| 12 |

J W Day Jr, C A Hall, A Yanez-Arancibia, D Pimentel, C I Marti, W J Mitsch (2009). Ecology in times of scarcity. Bioscience, 59(4): 321–331

https://doi.org/10.1525/bio.2009.59.4.10

|

| 13 |

J Diamond (2005). Collapse: How Societies Choose to Fail or Succeed.New York: Penguin,1–576

|

| 14 |

P R Ehrlich, A H Ehrlich (2009). The Dominant Animal: Human Evolution and the Environment. Washington D C: Island press, 480 p

|

| 15 |

P R Ehrlich, A H Ehrlich (2013). Can a collapse of global civilization be avoided? Proceedings of the Royal Society B: Biological Sciences, 280 (1754).

|

| 16 |

EIA (2002). Annual Energy Review 2001. Energy Information Administration : DOE/EIA-0384, 432p

|

| 17 |

EIA (2013). Annual Energy Outlook 2013. US DOE, 244p

|

| 18 |

EIA (2013a). Short-term Energy Outlook. Release Date: August 6, 2013, Energy Information Administration.

|

| 19 |

O Ekins, C Folke, R De Groot (2003). Identifying critical natural capital. Ecol Econ, 44(2 – 3): 159–163

https://doi.org/10.1016/S0921-8009(02)00271-9

|

| 20 |

El-Ashry M (2010). Renewables 2010 Global Status Report. Paris: REN21 Secretariat. Copyright Deutsche (GTZ) GmbH

|

| 21 |

M Fader, D Gerten, M Krause, W Lucht, W Cramer (2013). Spatial decoupling of agricultural production and consumption: quantifying dependences of countries on food imports due to domestic land and water constraints. Environmental Research Letters, 8 (1): 014046.

https://doi.org/10.1088/1748-9326/8/1/014046

|

| 22 |

J Farley, E Gaddis (2007). An ecological economic assessment of restoration. In: J Aronson, S Milton, J Blignaut eds. Restoring Natural Capital: Science, Business and Practice. Washington DC: Island Press

|

| 23 |

M T Firrisa, I van Duren, A Voinov (2013). Energy Efficiency for Rapeseed Biod iesel Production in Different Farming Systems. Energy Efficiency, 1–17 .

https://doi.org/10.1007/s12053-013-9201-2

|

| 24 |

L Gagnon, C Belanger, Y Uchiyama (2002). Life-cycle assessment of electricity generation options: the status of research in year 2001. Energy Policy, 30(14): 1267–1278

https://doi.org/10.1016/S0301-4215(02)00088-5

|

| 25 |

J Gever (1986). Beyond Oil (3rd edition). New York: Harper Business

|

| 26 |

K D Goldin (1975). Price externalities influence public-policy. Public Choice, 23(1): 1–10

|

| 27 |

J Gowdy, J Roxana (2005). Technology and Petroleum Exhaustion: Evidence from Two Mega-Oilfields. Rensselaer Working Papers in Economics

|

| 28 |

D L Greene (1997). Oil dependence: the value of R&D. Proceedings of the Intersociety Energy Conversion Engineering Conference. Volume 3, 2148–2153

|

| 29 |

D L Greene, J L Hopson, J Li (2004). Running out of and into oil: analyzing global oil depletion and transition through 2050. Energy and Environmental Concerns, 2004(1880): 1–9

|

| 30 |

L N Gumilev (1990). Ethnogenesis and the Biosphere. Moscow: Progress Publishers

|

| 31 |

C A S Hall, C J Cleveland, R Kaufmann (1986). Energy and Resource Quality: The Ecology of the Economic Process. New York: John Wiley and Sons

|

| 32 |

C A S Hall, J W Day (2009). Revisiting the limits to growth after peak oil In the 1970s a rising world population and the finite resources available to support it were hot topics. Interest faded-but it's time to take another look. Am Sci, 97(3): 230–237

https://doi.org/10.1511/2009.78.230

|

| 33 |

M Höök, R Hirsch, K Aleklett (2009). Giant oil field decline rates and their influence on world oil production. Energy Policy, 37(6): 2262–2272 .

https://doi.org/10.1016/j.enpol.2009.02.020

|

| 34 |

M K Hubbert (1950). Energy from fossil fuels. Washington D C, American Association for the Advancement of Science Centennial: 171–177

|

| 35 |

J D Hughes (2013). Energy: a reality check on the shale revolution. Nature, 494 (7437): 307–8 .

https://doi.org/10.1038/494307a

|

| 36 |

IEA (2007). Medium-Term Oil Market Report. L Eagles ed, International Energy Agency

|

| 37 |

IEA (2011). World Enegy Outlook. In IEA, 666

|

| 38 |

V Irastorza (2005). New metering enables simplified and more efficient rate structures. Electr J, 18(10): 53–61

https://doi.org/10.1016/j.tej.2005.10.008

|

| 39 |

C H Kahl (2006). States, Scarcity, Civil Strife in the Developing World. Princeton, NJ and Oxford: Princeton University Press

|

| 40 |

D S Kenney, C Goemans, R Klein, J Lowrey, K Reidy (2008). Residential water demand management: lessons from Aurora, Colorado. J Am Water Resour Assoc, 44(1): 192–207

https://doi.org/10.1111/j.1752-1688.2007.00147.x

|

| 41 |

R A Kerr (2008). Energy. World oil crunch looming? Science, 322(5905): 1178–1179

https://doi.org/10.1126/science.322.5905.1178

pmid: 19023054

|

| 42 |

P R Krugman (1979). Increasing returns, monopolistic competition, and international-trade. J Int Econ, 9(4): 469–479

https://doi.org/10.1016/0022-1996(79)90017-5

|

| 43 |

I Kubiszewski, C J Cleveland, P K Endres (2008). Energy return on investment (EROI) for wind energy. In: C J Clevelanded. Encyclopedia of Earth. last updated June 18, 2008

|

| 44 |

A Levermann, P U Clark, B Marzeion, G A Milne, D Pollard, V Radic, A Robinson (2013). The multimillennial sea-level commitment of global warming. Proceedings of the National Academy of Sciences (July 15): 1–6 .

https://doi.org/10.1073/pnas.1219414110

|

| 45 |

R G Lipsey, P N Courant, D D Purvis, P O Steiner (1993). Microeconomics (10th Edition). New York: Harper Collins College Publishers Inc

|

| 46 |

H A Loaiciga, S Renehan (1997). Municipal water use and water rates driven by severe drought: a case study. J Am Water Resour Assoc, 33(6): 1313–1326

https://doi.org/10.1111/j.1752-1688.1997.tb03555.x

|

| 47 |

T R Malthus (1826). An Essay on the Principle of Population. London: John Murray. Library of Economics and Liberty [Online]

|

| 48 |

M Meinshausen, N Meinshausen, W Hare, S C B Raper, K Frieler, R Knutti, D J Frame, M R Allen (2009). Greenhouse-gas Emission Targets for Limiting Global Warming to 2 °C. Nature, 458 (7242): 1158–1162

https://doi.org/10.1038/nature08017

|

| 49 |

K Mulder, N J Hagens (2008). Energy return on investment: toward a consistent framework. AMBIO: A Journal of the Human Environment, 37(2): 74–79

|

| 50 |

M Munasinghe, P Meier (1993). Energy Policy Analysis and Modeling. Cambridge: Cambridge University Press

|

| 51 |

D J Murphy, C Hall, B Powers (2010). New perspectives on the energy return on (energy) investment (EROI) of corn ethanol. Environment, Development and Sustainability, 13 (1): 179–202 .

https://doi.org/https://doi.org/10.1007/s10668-010-9255-14

|

| 52 |

J Murray, D King (2012). Climate policy: oil’s tipping point has passed. Nature, 481(7382): 433–435

https://doi.org/10.1038/481433a

pmid: 22281577

|

| 53 |

R K Pachauri, A Reisinger (2007). Climate Change 2007: Synthesis Report. Geneva, Switzerland, IPCC

|

| 54 |

W E Rees, M Wackernagel, P Testemale (1998). Our Ecological Footprint: Reducing Human Impact on the Earth. Gabriola Island: New Society Publishers

|

| 55 |

J L Simon (1998). The Ultimate Resource II. Princeton: Princeton University Press

|

| 56 |

S Solomon, G K Plattner, R Knutti, P Friedlingstein (2009). Irreversible climate change due to carbon dioxide emissions. Proc Natl Acad Sci USA, 106(6): 1704–1709

https://doi.org/10.1073/pnas.0812721106

pmid: 19179281

|

| 57 |

N Stern (2008). The Economics of Climate Change: The Stern Review. Cambridge: Cambridge University Press

|

| 58 |

A Trewavas (2002). Malthus foiled again and again. Nature, 418(6898): 668–670

https://doi.org/10.1038/nature01013

pmid: 12167872

|

| 59 |

A Voinov (2008). Systems Science and Modeling for Ecological Economics. Elsevier, Academic Press

|

| 60 |

J B. Whitcomb (2005). Florida water rates evaluation of single-family homes. Report to South Florida Water Management District: 113

|

|

Viewed |

|

|

|

Full text

|

|

|

|

|

Abstract

|

|

|

|

|

Cited |

|

|

|

|

| |

Shared |

|

|

|

|

| |

Discussed |

|

|

|

|